- Home

- Credit Score

- Axis Bank Cibil Score Csgen

Axis Bank CIBIL Score: How to Check and Improve Your Axis CIBIL Score

Why is your credit score significant? A strong credit score, ideally between 750 and 900, is a game-changer. It can speed up your loan approval, reduce interest rates, and smoothen your loan applications. Axis Bank even specifies the minimum credit score required for a home loan, personal loan, and credit card. So, carefully monitor your credit score—it can significantly open your doors to financial assistance when you need it the most!

- Instant Results

- No Hidden Fees

- Secure & Confidential

- No Impact on Your Credit Report

I agree to the Terms and Conditions of TUCIBIL and hereby provide explicit consent to share my Credit Information with Urban Money Private Limited.

Verify your number

Enter 6 Digit OTP

Change mobile number

Table of Content

Last Updated: 29 April 2026

How To Check Axis Bank CIBIL Score

To check your Axis Bank CIBIL Score, make sure to follow these steps:

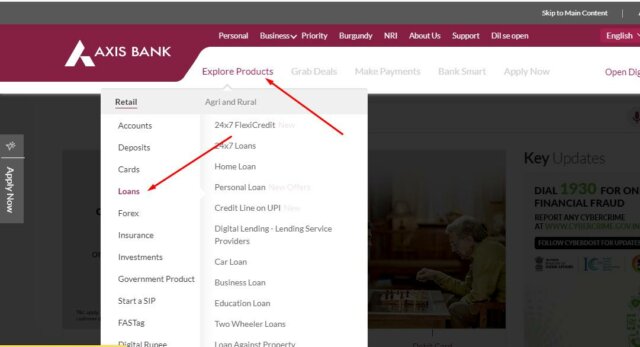

- Go to the official Axis Bank website.

- Navigate to “Explore Products” and select “Loans.”

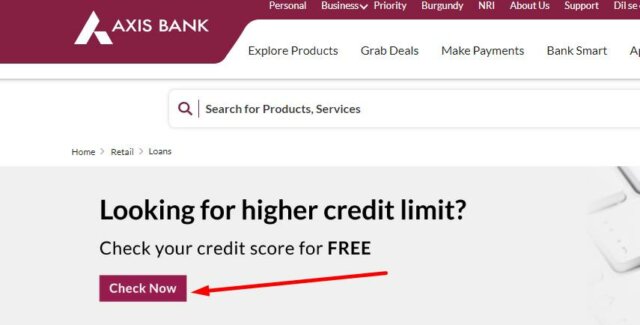

- Click on the Credit score banner.

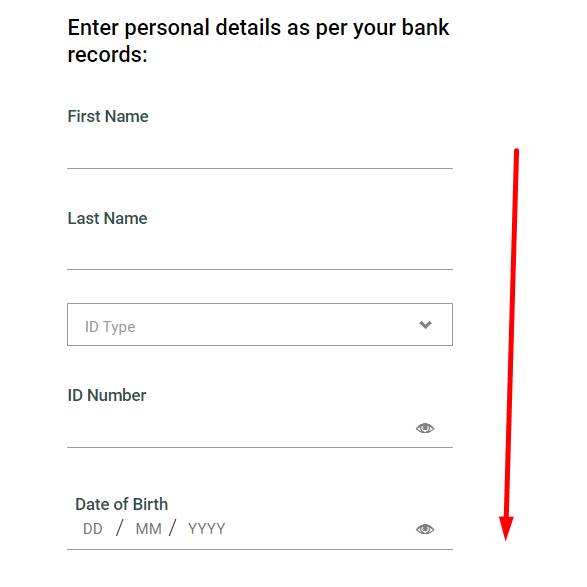

- Fill out the online form.

- Please enter your personal information, such as your email ID, name, date of birth, ID type, and mobile number.

- You will receive an OTP on your email address.

- Complete the registration process.

- Receive your complimentary credit report.

CIBIL Score for Axis Bank Home Loan

When you want to get a home loan from Axis Bank, your CIBIL score matters. Here’s the deal:

Your CIBIL score is like a report card of your borrowing history, with numbers from 300 to 900. The higher your score, the better you’ve handled credit in the past. But if it’s lower, there’s room to do better.

Axis Bank usually wants a home loan applicant with a score of at least 650. This number shows you are good at handling money and paying back what you owe. Moreover, your score also affects the interest you will pay on your loan. If your score is good, you will likely get a lower rate, saving you money in the long run. Other than that, a high CIBIL score might even get you a bigger loan than you requested. But if it’s low, you might not get as much as you hoped.

And here’s the kicker: if your score is high, you will probably get approved for your loan faster. But if it’s low, the bank might take longer to decide.

Axis CIBIL Score for Home Loan Eligibility

| Specification | Details |

| CIBIL Score | 750+ / 650-749 / <650 |

| Interest Rates | 8.50% – 9.50% |

| Processing Fees | 0.50% – 1% (Min: ₹10,000) |

| Prepayment | Floating: Nil / Fixed: Up to 2% |

| Loan Tenure | 5 to 30 years |

| Loan Amount | Min: ₹3 lakh / Max: ₹5 crore |

| Age | 21 to 65 years |

| Insurance | Required |

| Disbursement | 15-30 days |

| LTV | Max: 90% |

CIBIL Score for Axis Bank Personal Loan

Your CIBIL score is crucial to establish mutual trust between you and your lenders. It showcases how reliable you are with money by reflecting on your borrowing and repayment history. Lenders rely on your credit score to decide whether to give you that loan or establish strict rules to ensure timely repayments. Ideally, aim for a CIBIL score of 710 or higher. It increases your chances of loan approval and can give you better terms, like lower interest rates and more favorable conditions. But what if your score is lower, say around 600? Well, it’s a bit of a grey area. Some lenders might still consider scores under 710, but usually, they come with a catch—higher interest rates. It’s always good to check directly with the lender to see where you stand.

Now, what shapes your CIBIL score?

- First off, making timely payments is a huge plus. Paying your bills on time is like a gold star for your score.

- Also, keep your credit card spending in check. It’s better for your score if you don’t max out your cards.

- Lenders also consider how long you’ve been borrowing money. The longer your credit history, the better it looks on your record.

And here’s a tip: having a mix of different loans—like a home loan and a credit card—can boost your score. But watch out for credit inquiries. Every time you apply for a loan or a credit card, it leaves a mark on your record. Too many marks can temporarily bring your score down.

Axis CIBIL Score for Personal Loan Eligibility

| Specification | Details |

| CIBIL Score | 750+ / 700-749 / <700 |

| Interest Rates | 10% – 24% |

| Processing Fees | 1% of loan amount (Min: ₹10,000) |

| Prepayment | Floating: Nil / Fixed: Up to 2% |

| Loan Tenure | 1 to 5 years |

| Loan Amount | Min: ₹15,000 / Max: ₹25 lakh |

| Age | 21 to 60 years |

| Insurance | Optional |

| Disbursement | Within 3-5 days |

| LTV | N/A |

CIBIL Score Required for Axis Bank Credit Card

The applicant must have a decent credit score to be eligible for an Axis Bank credit card if the applicant’s borrowing and repayment history indicates that the applicant does not have a good repayment history.

The CIBIL Score required to qualify for an Axis Bank Credit Card is a minimum of 650 or higher. Holding a higher score allows the bank to develop mutual trust and increases your chances of securing a credit card with a generous spending limit. Occasionally, Axis Bank might consider issuing a credit card even if your score falls below this benchmark, particularly if you have a regular and healthy income and maintain a favourable debt-to-income ratio.

If your credit score is lower than expected, you still have a chance to avail of a credit card, but the eligibility criteria can become stringent. Thus, it is always advisable to hold a healthy credit score so that you can avail yourself of a credit card from any bank at any time.

What are the Factors Affecting Your Axis Bank CIBIL Score

Your CIBIL score is a crucial factor lenders look at when you’re applying for loans or credit cards. Let us take a look at the important factors that affect your cibil score:

- Payment History (35%): This is an important factor that affects your cibil score significantly. It shows if you are good at paying bills on time. Late payments or defaults can hurt your score, but being consistent helps.

- Credit Utilisation Ratio (30%): This is about how much of your credit you use compared to what you are given. Using too much can lower your score, so it’s smart to keep it low.

- Duration of Credit History (15%): The longer you have been using credit responsibly, the better it is for your score. New credit card users might have lower scores because they haven’t built enough history yet.

- Credit Mix and Variety: Having a mix of different types of credit, like loans and credit cards, can be good for your score. It shows you can handle different kinds of debt responsibly.

- Number of Credit Inquiries: Every time you apply for credit, it leaves a mark. Too many marks can bring your score down temporarily, so it’s best to keep applications to a minimum.

Range Table of Axis Bank CIBIL Score

Let us take a look at the table below to understand the different ranges of CIBIL scores and the category to which each range belongs:

| CIBIL Score | Interpretation |

| 300-549 | Poor Score: High risk to lenders |

| 550-699 | Average Score: Repayment hurdles but potential for improvements. |

| 700-749 | Good Score: A decent credit score reflecting responsible credit behaviour. |

| 750+ | Excellent: Qualifies for better loan deals |

Steps to Improve Your Low Axis Bank Credit Score

A below-average credit score indicates irresponsibility towards repayments, which results in the inability to establish trust between the applicant and the lender. If you have a below-average credit score and wish to improve it, here are the ways to improve your Axis Bank credit score:

- Timely Repayments: Pay your EMIs well before the due date. If you cannot pay on time, an interest rate will apply to the defaulted payments, lowering your credit score. Hence, timely repayments are crucial to maintaining or improving your credit score.

- Settle Your Past Dues: If you have any credit outstanding, make sure you pay that on time. Spending more than your budget and unable to pay your EMIs will result in consolidated debt, lowering your credit score significantly.

- Wise Usage of Credit Cards: Spending too much than required, knowing it exceeds your budget and might result in defaulted repayments, is not wise. Hence, take note of your budget and realise the maximum EMI you can afford to pay. Also, timely repayments are crucial. Therefore, moderate usage with timely repayments is one of the best ways to improve your credit score.

Latest from the Credit Score Blog

Get in-depth knowledge about all things related to Credit Score and your finances

crif-high-mark-dispute-resolution

Common Errors Found in CRIF High Mark Credit Reports Here are the common errors found in CRIF High Mark credit reports: Closed Accounts Showing as Open: Accounts you have paid off may still appear open. This can affect

Why Checking Your CIBIL Score is Crucial Before Applying for a Loan

Understanding CIBIL Score A CIBIL score is a three-digit number that shows how responsible you are with money and credit. It ranges from 300 to 900, with a higher score meaning you handle credit well. Credit Information

How Gold Loans Affect Your CIBIL Score and Tips to Protect It

Does Taking a Gold Loan Affect Your CIBIL Score? The short answer is yes, it does. However, whether the impact is positive or negative depends entirely on how you manage your gold loan. When you take out a gold loan, you

Managing CIBIL Score and Financial Emergencies

Understanding CIBIL Score Basics A CIBIL score is a three-digit number between 300 and 900 that shows your creditworthiness. It is based on your credit history, which includes how you have handled loans and credit cards.

Role of CIBIL Score in Car Loan Approval and Terms

How CIBIL Scores Influence Car Loan Approval? The CIBIL score is a three-digit number that ranges between 300 and 900. A higher score indicates better creditworthiness and vice versa. Lenders typically prefer applicants

Kotak CIBIL Score: How to Check & Loan Requirements

How to Check Your Kotak CIBIL Score? Checking your CIBIL score regularly is crucial for maintaining a healthy credit profile. Here is a step-by-step details to checking your Kotak CIBIL score: Visit the Official CIBIL W

CIBIL Score for Car Loans: Top Picks for 2024

List of Best Car Loan in India 2024 Here are some of the best available car loan options in India with minimal interest rates and low processing fees: State Bank of India Car Loan SBI offers a fantastic deal to finance

Does Checking Your CIBIL Score Impact Your Credit Score?

Does Checking Your CIBIL Score Affect It? True or False? The short answer is false. Checking your CIBIL score is considered a soft inquiry and does not impact your credit score. People often get confused because they fai

How to Avoid Credit Repair Scams and Protect Your Credit Score

Understanding Credit Repair Scams Credit repair scams are traps set by individuals into luring you by offering you a magical solution that practically holds no meaning. They use sneaky tricks to make you believe they can

Difference Between Equifax & CIBIL Score

Equifax Vs CIBIL Understanding credit scores is paramount for securing loans and credit cards in India. Equifax and CIBIL (TransUnion CIBIL) are prominent players in this arena. While both provide credit information to l

How Student Loans Influence Your Credit Score

The Impact of Student Loans on Your Credit Score The impact of education loans on CIBIL scores can be positive and negative. As mentioned above, the outcome largely depends on managing your credits. For a more detailed i

How Bankruptcy Impacts Your Credit Score

Impact of Bankruptcy on Your Credit Score Here are the key aspects of how bankruptcy impacts on your credit score and beyond: 1. Significant Drop in Credit Score Your credit score takes a massive hit when you file for ba

Best CIBIL Score For Loans

Maintaining a good CIBIL score for a loan can ensure you access the financial help you need quickly and on favourable terms. Understanding and improving your CIBIL score can open doors to better financial opportunities,

Low Credit Score Personal Loans: How to Get Approved Fast

Different Ways To Get Personal Loan on Low CIBIL Here are some strategies you can use to increase your chances of approval: Borrow smart: Opt for a smaller loan amount. This reduces the risk for the lender and makes the

Credit Counseling and Financial Education in India

Understanding Credit Counseling Credit counselling is valuable for individuals seeking to manage and pay down debt. It’s a structured process facilitated by certified credit counselling agencies like Urban Money. These a